How to stay hawkish in New Zealand

Hi everyone, sorry about the delay in writing this post I have had a flu and so have fallen behind in all my work including this.

The first order of business is to discuss Thursday’s employment data, something I said I would do on Thursday. However, instead of sticking to the popular indication of what it means I’m going to run with an alternative interpretation – the hawkish view of the employment data. Furthermore, I will use this to come up with a hawkish interpretation of the New Zealand economic situation.

Note that this interpretation is an exercise to make us think about exactly what is going on in the economy – I’m not saying that this is the most realistic interpretation, but it is useful to go through and discuss nonetheless.

Eric Crampton foreshadowed this potential interpretation in his insightful comment to this post. In the comment he discusses working for families and a reduction in labour supply in the economy, this is what is called an negative Aggregate Supply shock.

There are two types of aggregate supply (AS) shocks we need to look at for all intensive purposes, short-run AS shocks (temporary shocks that are reversed) and long run AS shocks (shocks that are not reversed, so are permanent).

Labour shocks

Our participation rate has grown strongly in recent years, indicating that there has been a positive AS shock (this of course assumes that our participation rate is unbiased, which it is not – it seems to be positively correlated with employment growth. This is a big issue, but one we will abstract from for now). How is this a positive AS shock? Well labour is a resource that can be used to create goods. If the participation rate rises we have had an increase in the labour resource (an increase in labour supply), which in turn implies that we can create more goods.

However, the pull-back in employment over the March quarter was met with a large reduction in the participation rate. This indicates that we experienced a negative AS shock in March.

The question then is – is this a temporary or permanent shock. If we believed that working for families was the reason for the adjustment in the March quarter, then it would be fair to assume that this is a “permanent shock”, as working for families is a permanent policy. Although it is unlikely that the March change was solely the result of WFF, it is not inconceivable that this, in combination with our aging population profile are major candidates for continued permanent AS shocks in New Zealand.

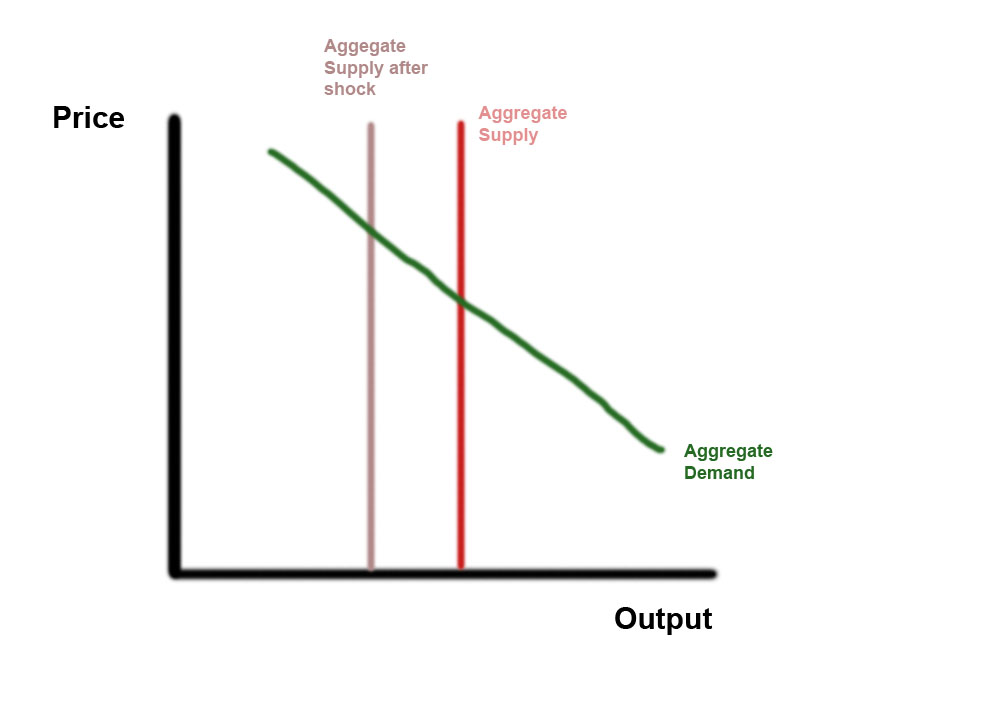

Now a permanent shock reduces the long-run aggregate supply curve of the economy (LAS). The impact of this looks like the following graph.

This tells us that when there is a permanent reduction in aggregate supply, the price level will be higher and output in the economy will be lower. As the Reserve Bank controls the interest rate, which moves aggregate demand, they can’t bring us back to the level of output we as an economy have been accustomed to – instead all they can do is increase the price level.

In other words, the shift in LAS has reduced “potential output” in the economy. If the RBNZ does not adjust for the reduction in potential output when making its interest rate choice (given that they use an output-gap model) they will under-forecast inflation. As there is no long-run trade-off between inflation and output, such an action will simply mean higher inflation over time!

Other shocks

A potential labour market aggregate supply shock is not the only shock we have experienced. Higher oil prices, increased compliance costs, higher input costs, and he drought all constitute as negative aggregate supply shocks.

However, excluding the potential for “peak oil” these shocks mainly constitute temporary, or short-run aggregate supply shocks. In this case output has been decreased below the “potential rate”, and Reserve Bank policy can be used to bring the economy closer to its “potential rate” at the cost of a higher price level and short-term inflationary pressures.

Furthermore, it is important to note that short-term supply shocks will increase the price level. If consumers or firms get “confused” and assume that this increase in the price level is actually inflation (which appears to be a fair assumption given how long we have sat at the top of our inflation band) this shock may feed into inflation expectations – and therefore into medium term inflation itself. As a result, even if the RBNZ does believe in an output gap based model, the chance of a forward looking based inflation spiral is something they have to take into account – even when looking at these short-run supply shocks.

But – we should be as well off as before, surely

The issue with supply shocks is that they reduce the actual number of goods and services we can allocate, distribute, and trade through society. Ultimately, people have to be willing to make sacrifices when something like this occurs.

If you accidentally dropped your wallet and lost a couple of thousand dollars it is likely that you would reduce the amount you consumed (I know I would). An AS shock is similar – we have lost some of our income, and we just have to accept that we won’t be as well off until we get some positive AS shocks.

How does this let us be hawkish? Well if the RBNZ’s mandate is to truly control inflation, then it must be willing to look past the temporary supply shocks and to take into account any permanent ones. If we believe the labour market data is telling us that labour supply is falling – then it is evidence that the Bank must be stronger on inflation, not weaker.

However, it is far more likely that the Bank will see this data as indicative of weakening labour demand – something that will bring it closer to cutting rates over the next six months.

I have no technical disagreements Matt. I would note that:

a) the overall terms of trade would suggest a positive supply shock

b) it’s hard to dismiss the possibility that we have just experienced a negative shock to aggregate demand. March quarter consumption and net exports look flat or negative, and business surveys don’t offer much hope for investment. Thank heavens for government spending! 🙂

On female labour force participation: that series has been wobbling around for the last 4 quarters, I don’t see much of a trend. It would be hard to disentangle the WFF effect from the demographics – I’ve seen work suggesting that the lift in female participation was about to come to an end anyway. Also WFF had some positive work incentives for beneficiaries, so the net results were always going to be a little ambiguous.

If (big if) we believe the HLFS i think that rising unemployment and falling employment rates is a convincing sign of an easing labour market and hence evidence in favour of lower interest rates, although I accept the argument that it could be taken as an early indicator of a permanently lower rate of labour force growth (and thus a sign that there is going to be more inflation pressure).

Hi CPW,

Thanks for raising the other side – I don’t really have the time to post the dovish interpretation 😛

It will be interesting to see what happens – but I agree that with the current set of information its damn hard to make a call either way. I also agree that the Reserve Bank will take this as a sign to cut rates.

To get the effect of WFF properly, you’d need a rather specialized CURF from Stats NZ. Basically, you need to know whether women subject to treatment had a differential labour supply response to women not subject to treatment: so, you need to know family income and number of children as well as individual hours worked. I don’t have that data. Sigh.